RULES & REGULATIONS

TERMS AND CONDITIONS OF YOUR DEPOSIT ACCOUNT

We are a healthy, growing, locally-owned, independent bank working to improve our community of Atlantic, Iowa.

Dear Depositor:

This brochure contains the rules which govern, where appropriate, your deposit account with us. Please read this brochure carefully; continued use of your account with us after receipt of this brochure means you agree to these rules, you agree to pay the fees listed and you give us the right to collect the fees, as earned, directly from the account balance. If you have any questions, please call us.

Much of our relationship with our deposit customers is regulated by state and federal law, especially the law relating to negotiable instruments, the law regulating the methods of transferring property upon death and the rights of surviving spouses and dependents, the law pertaining to estate and other succession taxes, the law regarding electronic funds transfer, and the law regarding the availability of deposited funds.

We may permit some variations from this standard agreement, but any such variations must be agreed to in writing either on our signature card for the account or in some other written form.

As used in this brochure, the word “we” means the financial institution and the word “you” means the account holder.

DEPOSITS & WITHDRAWALS

Any customer may make deposits in the account at any time. If the account is a joint account, any one of the customers may withdraw the entire balance and we are not required to make any inquiry or determination as to the use of the money so withdrawn. If the account is a common account, we may permit customer to withdraw funds by the number and identity of the customer. We are not required to make any inquiry or determination as to the use of the money so withdrawn. If the account is a payable on death or trust account, only the customer indicated may make withdrawals during his lifetime. Thereafter, the designated beneficiary may withdraw any money left in the account. If the account is any other type of account, customer may withdraw funds by the number and identity of the customer(s).

Withdrawals may be made by check or other forms furnished by us. If the account is a savings, certificate of deposit, HiFi or NOW account, we reserve the right to require 14 days notice of any withdrawal. If it is a Super Now account, we reserve the right to require 7 days notice of withdrawal. If it is another type of account, we reserve the right to require such notice of withdrawal as may be required by regulation or law.

Deposits, other than in cash, will be handled as follows. We are the customer’s agent as to all such deposits and are required only to act with due care as to them. We may give credit for such deposits when they are made or may withhold credit until the deposit is actually paid to us. If we give credit when the deposit is made, we may withdraw or revoke such credit at any time before it is actually paid to us. We may forward such deposits to other banks, including the Federal Reserve Bank, and will not be liable for any failure by such bank to exercise due care or make payment to us. We may handle any such deposit in accordance with Federal Reserve requirements.

We may, at any time, apply all or any part of the balance in the account to the payment of any amount owed to us by any customer entitled to make withdrawals from the account.

The account may be subject to service charges or other fees assessed by us from time to time. Such service charges or fees, if any, will be assessed by us uniformly on all accounts of this type.

We will furnish customer with a statement of the account from time to time. Such statements and any other notices may be given to any customer.

TRUST AND PAY-ON-DEATH ACCOUNTS

Except as such an account may be varied by a separate agreement: (1) the person opening a Trust or Pay-on-Death account (called the “settlor”) may withdraw all or any portion of the account balance during his lifetime; (2) any named beneficiary who does not sign the signature card acquires the right to withdraw from the account only if and when he survives the settlor; and (3) if more than one beneficiary is named and survives, the interest of such surviving beneficiaries shall be in equal shares and without survivorship between them.

JOINT ACCOUNT – WITH SURVIVORSHIP

If such an account is indicated on our signature card, each joint tenant intends and agrees that the account balance upon his death shall be the property of the surviving joint tenant, and if more than one survives, they shall remain as joint tenants with right of survivorship between them.

AMENDMENTS AND TERMINATION

We may amend any term of this agreement, from time to time hereafter, upon giving reasonable notice to you. Reasonable notice may consist of posting notice of such changes in our building for a reasonable period of time, enclosing notice in the statement of this account, or separate notice by mail. We may also close this account at any time upon reasonable notice to you and tender of the account balance personally or by mail. Notice from us to any one of you is notice to all of you.

DIRECT DEPOSITS

If, in connection with a direct deposit plan, we deposit any amount in this account which should have been returned to the Federal Government for any reason, you authorize us to deduct the amount of our liability to the Federal Government from this account or from any other account you have with us, without prior notice and at any time, except as prohibited by law. We may also use any other legal remedy to recover the amount of our liability.

ELECTRONIC FUND TRANSFERS

Your Rights and Responsibilities

The Electronic Fund Transfers we are capable of handling for consumers are indicated below, some or all of which may apply to your account. Please read this disclosure carefully because it tells you your rights and obligations for these transactions. You should keep this notice for future reference.

1. TYPES AND LIMITATIONS OF TRANSFERS

Terminal Transfers -Terminals are equipped to handle:

• Cash withdrawals from checking accounts.

• Cash withdrawals from savings accounts.

• Deposits to checking accounts.

• Deposits to savings accounts.

• Transfers of funds between checking and savings accounts upon request.

Some of the services may not be available at all terminals.

Prearranged Transfers – We are equipped to:

• Accept certain direct deposits to your checking account.

• Accept certain direct deposits to your savings account.

• Pay certain recurring bills from your checking account.

• Pay certain recurring bills from your savings account.

Electronic Fund Transfers Initiated By Third Parties. You may authorize a third party to initiate electronic fund transfers between your account and the third party’s account. These transfers to make or receive payment may be one-time occurrences or may recur as directed by you. These transfers may use the Automated Clearinghouse (ACH) or other payments network. Your authorization to the third party to make these transfers can occur in a number of ways. In some cases, your authorization can occur when the merchant posts a sign informing you of their policy. In all cases, the transaction will require you to provide the third party with your account number and bank information. This information can be found on your check as well as on a deposit or withdrawal slip. Thus, you should only provide your bank and account information (whether over the phone, the Internet, or via some other method) to trusted third parties whom you have authorized to initiate these electronic fund transfers.

Examples of these transfers include, but are not limited to:

• Electronic check conversion. You may provide your check to a merchant or service provider who will scan the check for the encoded bank and account information. The merchant or service provider will then use this information to convert the transaction into an electronic fund transfer. This may occur at the point of purchase, or when you provide your check by other means such as by mail or drop box.

• Electronic returned check charge. Some merchants or service providers will initiate an electronic fund transfer to collect a charge in the event a check is returned for insufficient funds.

Limitations on savings accounts

No more than six electronic transfers and withdrawals, or a combination of such transfers and withdrawals, per calendar month or statement cycle (or similar period) of at least four weeks, to another account (including a transaction account) of the depositor at the same institution or to a third party by means of a preauthorized or automatic transfer, or telephonic (including data transmission) agreement, order or instruction, or by draft, debit card, or similar order made by the depositor and payable to third parties. (12 CFR 204.2(d)(2))

FDIC Deposit Insurance Coverage

Your money is SAFE with our deposit insurance at no cost to you. This insurance protection is provided by an independent agency of the United States Government. The standard maximum deposit insurance is $250,000 per depositor at any one financial institution.

1. DOLLAR LIMIT ON TERMINAL TRANSFER

• The total limit is $200.00 per business day.

2. CHARGES FOR ELECTRONIC FUND TRANSFERS

(A.) We do not charge for direct deposits to any account except

credit to non-personal accounts.

(B.) We charge $10.00 per card each year to customers whose accounts are set up to use ATM Cards.

(C.) Withdrawals through an electronic funds transfer service will be charged the same as a check if your account is subject to service charges.

(D.) You receive 4 free withdrawals per card number per statement cycle. Additional withdrawals $1.00 each.

(E.) Transfers initiated by Automatic Transfer System will be charged $3.50 per transaction.

Except as indicated above, we do not charge for Electronic Fund Transfers. Access fees may be charged when customer uses an ATM not operated by this bank.

3. RIGHT TO DOCUMENTATION

(A.) Terminal Transfers. You can get a receipt for transactions in excess of $15 at the time you make any transfer to or from your account.

(B.) Direct Deposits. If you have arranged to have direct deposits made to your account at least once every 60 days from the same person or company, you can call us at the telephone number listed in section 9 to find out whether or not the deposit has been made.

(C.) In Addition.

(I.) You will receive a monthly account statement from us on your checking, Now, and Super Now accounts.

(2.) You will receive a monthly account statement from us on your savings accounts unless there are no transfers in a particular month. In that case, you will get a statement quarterly.

4. STOP PAYMENT PROCEDURES AND NOTICE OF VARYING AMOUNTS

(A.) Right to stop payment and procedure for doing so. If you have told us in advance to make regular payments out of your account, you can stop any of these payments. Here’s how:

Call or write us at the telephone number or address listed in section 9, in time for us to receive your request 3 business days or more before the payment is scheduled to be made. If you call, we may also require you to put your request in writing and get it to us within 14 days after you call, or the verbal stop payment will cease to be binding.

(B.) Notice of varying amounts. If these regular payments may vary in amount, the person you are going to pay will tell you, 10 days before each payment, when it will be made and how much it will be.

(C.) Liability for failure to stop payment of preauthorized transfer. If you order us to stop one of these payments 3 business days or more before the transfer is scheduled, and we do not do so, we will be liable for your losses or damages, as long as the information you provided was exact.

5. FINANCIAL INSTITUTION’S OBLIGATIONS

(A.) Liability for failure to make transfers. If we do not complete a transfer to or from your account on time or in the correct amount according to our agreement with you, we will be liable for your losses or damages, However, there are some exceptions. We will not be liable, for instance:

• If, through no fault of ours, you do not have enough money in your account to make the transfer.

• If the automated teller machine where you are making the transfer does not have enough cash.

• If the terminal or system was not working properly and you knew about the breakdown when you started the transfer.

• If circumstances beyond our control (such as fire or flood) prevent the transfer, despite reasonable precautions that we have taken.

• There may be other exceptions stated in our agreement with you.

6. DISCLOSURE TO THIRD PARTIES

(A.) Account Information disclosure. We will disclose information to third parties about your account or the transfer you make.

(1.) where it is necessary for completing transfers; or

(2.) in order to verify the existence and condition of your account for a third party, such as a credit bureau or merchant; or

(3.) in order to comply with government agency or court orders; or

(4.) if you give us your written permission.

7. UNAUTHORIZED TRANSFERS

(A.) Liability disclosure. Tell us AT ONCE if you believe your card has been lost or stolen. Telephoning is the best way to keep your possible losses down. If you do give us notice of a lost or stolen card within 2 business days, you will be liable for the lessor (1) $50.00 or (2) the amount of any money, property or services obtained by its unauthorized use prior to the time you gave us notice. If you do not notify us within 2 business days, your liability could be as high as $500.00.

Also, if your statement shows transfers that you did not make, tell us at once. If you do not tell us within 60 days after the statement was mailed to you, you may not get back any money you lost after the 60 days if we can prove that we could have stopped someone from taking the money if you told us in time.

If a good reason (such as a long trip or a hospital stay) kept you from telling us, we will extend the time periods.

(B.) Address and telephone number. If you believe your card has been lost or stolen or that someone has transferred or may transfer money from your account without your permission, call or write us at the telephone number or address listed in section 9.

8. ERROR RESOLUTION

In case of errors or questions about your electronic transfers, call or write us at the telephone number or address listed in section 9, as soon as you can, if you think your statement or receipt is wrong or if your need more information about a transfer listed on the statement or receipt. We must hear from you no later than 60 days after we sent the FIRST statement on which the problem or error appeared.

(1.) Tell us your name and account number (if any)

(2.) Describe the error or the transfer you are unsure about, and explain as clearly as you can why you believe it is an error or why you need more information.

(3.) Tell us the dollar amount of the suspected error.

If you tell us orally, we may require that you send us your complaint or question in writing within 10 business days.

We will determine whether an error occurred within 10 business days (20 business days if the transfer involved a new account) after we hear from you and will correct any error promptly. If we need more time, however, we may take up to 45 days (90 days if the transfer involved a new account, a point-of-sale transaction, or a foreign-initiated transfer) to investigate your complaint or question. If we decide to do this, we will credit your account within 10 business days (20 business days if the transfer involved a new account) for the amount you think is in error, so that you will have the use of the money during the time it takes us to complete our investigation. If we ask you to put your complaint or question in writing and we do not receive it within 10 business days, we may not credit your account. An account is considered a new account for 30 days after the first deposit is made, if you are a new customer.

If we decide that there was no error, we will send you a written explanation within 3 business days after we finish our investigation. You may ask for copies of the documents that we used in our investigation.

Limits on Liability for MasterCard © debit card. You will not be liable for any unauthorized transactions using your MasterCard © debit card, if you can demonstrate that you have exercised reasonable care in safeguarding your card from the risk of loss or theft, and upon becoming aware, report the loss or theft to us within 2 business days. If this condition is not met, your liability could be up to $500 if not reported in 2 business days and unlimited liability if the unauthorized transaction is not reported within 60 days of when the unauthorized transaction was on a periodic statement.

Advisory Against Illegal Use. You agree not to use your card(s) for illegal gambling or other illegal purpose. Display of a payment card logo by, for example, an online merchant does not necessarily mean that transactions are lawful in all jurisdictions in which the cardholder may be located.

9. OUR BUSINESS DAYS ARE MONDAY – FRIDAY

1ST WHITNEY BANK AND TRUST

ATLANTIC, IOWA

223 CHESTNUT STREET

PH. 712-243-3195

700 CHESTNUT STREET

PH. 712-243-4183

YOUR ABILITY TO WITHDRAW FUNDS

Our policy is to make funds from your deposits to transaction accounts available to you on the first business day after the day we receive your deposit. At that time, you can withdraw the funds in cash and we will use the funds to pay checks that you have written.

For determining the availability of your deposits, every day is a business day, except Saturdays, Sundays, and federal holidays. If you make a deposit before 3:00 P.M. on a business day that we are open, we will consider that day to be the day of your deposit. However, if you make a deposit after 3:00 P.M. or on a day we are not open, we will consider that the deposit was made on the next business day we are open.

LONGER DELAYS MAY APPLY

In some cases, we will not make all of the funds that you deposit by check available to you on the first business day after the day of your deposit. However, Cash and Electronic Deposits will be available the first business day after we receive your deposit for withdrawal and to pay checks that you have written. For other deposits, depending on the type of check that you deposit, funds may not be available until the second business day. In this case, the first $225 of your deposit will be available on the first business day.

If we are not going to make all of the funds from your deposit available on the first business day, we will notify you at the time you make your deposit. We will also tell you when the funds will be available. If your deposit is not made directly to one of our employees, or if we decide to take this action after you left the premises, we will mail you the notice by the day after we receive your deposit.

If you will need the funds from a deposit right away, you should ask us when the funds will be available.

In addition, funds you deposit by check may be delayed for a longer period under the following circumstances:

We believe a check you deposit will not be paid.

You deposit checks totaling more than $5,525 on any one day.

You redeposit a check that has been returned unpaid.

You have overdrawn your account repeatedly in the last six months.

An emergency, such as failure of communications or computer equipment has occurred.

We will notify you if we delay your ability to withdraw funds for any of these reasons, and we will tell you when the funds will be available. They will generally be available no later than the 7th business day after the day of your deposit.

For deposits into new accounts (less than 30 days old), cash, electronic deposits and the first $5,525 of any U.S. Postal Service money orders, Federal Reserve Bank Checks, State or General Local Government Checks, Cashiers, Certified or Teller Checks and “On Us” checks will be available the first business day after the deposit.

The excess over $5,525, as well as all other checks will be available on the 7th business day after the day of your deposit.

PERSONAL CHECKING

Your First Whitney Bank checking account provides an easy bookkeeping record of purchases and paid bills, and your cancelled checks are proof of payment. You always have a precise accounting of just how much money you have spent, when, and where. A complete statement of your account is sent to you every month.

ATM and banking by mail is available. See us for further details. Each depositor is insured to $250,000 by the Federal Deposit Insurance Corporation.

FIVE SERVICE PLANS ARE AVAILABLE

1. Pay as you check.

2. Regular checking

3. Banclub

4. Now Accounts

-Your interest rate and annual percentage yield may change. At our discretion, we may change the interest rate on your account daily. The interest rate for your account will never be less the 0.00%

-Interest begins to accrue on the business day you deposit noncash items (for example, checks).

-Interest is compounded and credited monthly. If you close your account before interest is credited, you will receive the accrued interest.

-We use the daily balance method to calculate the interest on your account. This method applies a daily periodic rate to the principal in the account each day.

5. Super Now Accounts

-Your interest rate and annual percentage yield may change. At our discretion, we may change the interest rate on your account daily. The interest rate on your account will never be less than 0.00%.

-Interest begins to accrue on the collected balances (noncash items, check, may take up to two business days).

-Interest is compounded and credited monthly. If you close your account before interest is credited, you will receive the accrued interest.

-We use the daily balance method to calculate the interest on your account. This method applies a daily periodic rate to the principal in the account each day.

BUSINESS CHECKING

Provides all of the advantages of a regular checking for record keeping, convenience of payment, safety, and IRS records. Various check forms are available for specific purposes and businesses. Interest earned on qualified balances is credited to offset service charges.

SAVINGS ACCOUNTS

A savings account can be one of your most valuable assets. Every sound financial program is based on a savings account. Whatever your savings needs may be – retirement, education, vacation, or simply the secure feeling of money in the bank – we have a savings plan that is right for you.

FLEXIBLE SAVINGS PLANS.

At First Whitney Bank & Trust, you can choose from a wide variety of flexible savings plans that keep your money working for you.

PASSBOOK SAVINGS

-Interest begins to accrue on the business day you deposit noncash items (for example, checks).

-Interest is compounded and credited on the last day of each quarter. If you close your account before interest is credited, you will receive the accrued interest.

We use the daily balance method to calculate the interest on your account. This method applies a daily periodic rate to the principal In the account each day.

-This account is restricted to six (6) electronic withdrawals or transfers per month cycle.

-The interest rate is subject to change at the bank’s discretion.

HIFI SAVINGS AND WHITNEY PLUS

-Your interest rate and annual percentage yield may change. At our discretion, we may change the Interest rate on your account daily. The interest rate on your account will never be less than 0.00%.

-You may make six (6) electronic withdrawals or transfers from your account per statement cycle.

-Interest is compounded and credited monthly. If you close your account before the interest is credited, you will receive the accrued interest.

-We use the daily balance method to calculate the interest on your account. This method applies a daily periodic rate to the principal in the account each day.

-Interest begins to accrue on the collected balances (noncash items, checks, may take up to two business days).

CERTIFICATES OF DEPOSIT

-Interest can be withdrawn prior to maturity. If interest is withdrawn prior to maturity, your annual percentage yield will be reduced.

-The interest rate for your account will be paid until the maturity date of your certificate.

-Interest begins to accrue on the business day you deposit noncash items (for example, checks).

-This account will automatically renew at maturity. You will have ten (10) calendar days from the maturity date to withdraw your funds without being charged a penalty.

-After the account is opened, you may not make deposits into or withdrawals from this account until the maturity date.

-We use the daily balance method to calculate the interest on your account. This method applies a daily periodic rate to the principal in the account each day.

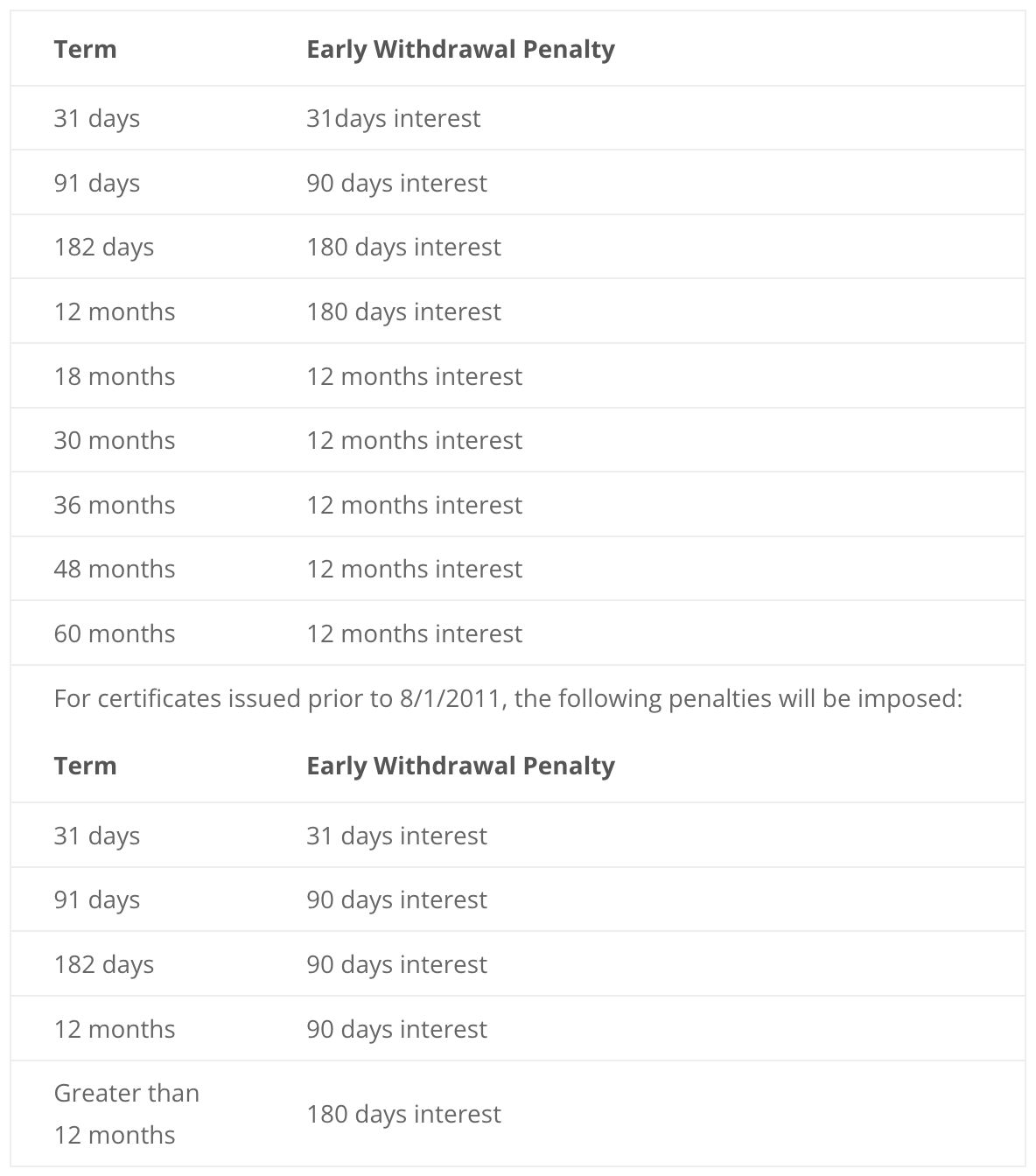

-If any of the deposit is withdrawn before the maturity date, a penalty as shown below will be imposed:

Special Certificates may be available. Maturity and penalty varies.

-The interest rate for your account will be paid up to five (5) days past maturity date of your certificate.

-Interest is compounded semi-annually and will be credited to your account semi-annually.

-If the certificate’s term is less than 182 days, the interest will be compounded and credited to your account at its maturity.

-Interest can be withdrawn prior to maturity. If interest is withdrawn prior to maturity, your annual percentage yield will be reduced.

LOAN SERVICES

- Ag Loans

- Business Loans

- Personal Loans

- Auto Loans

- Installment Loans

- Home Improvement Loans

- Real Estate Loans

- Small Business Administration Loans

AUTOMATIC LOAN PAYMENTS

Loan payments can be accomplished by automatic withdrawal from the account.

OVERDRAFT CHECKING

CUSTOMER OVERDRAFT POLICY

An Insufficient balance could result in several ways, such as: a) the payment of checks, electronic funds transfers, or other withdrawal requests; b) payments authorized by you; c) the return of unpaid items deposited by you; d) the assessment of bank service charges; or e) the deposit of items which, according to the bank’s Funds Availability Policy, are treated as not yet available or finally paid. We are not obligated to pay any item presented for payment if your account does not contain sufficient funds. Rather than automatically returning, unpaid, any non-sufficient funds items that you have, if your eligible account is in good standing, which includes at least: a) you are not in default on any loan obligation to First Whitney Bank & Trust, b) you bring your account to a positive balance (not overdrawn) at least once every fifteen (15) calendar days, and c) your account is not the subject of any legal or administrative order or levy, we will consider – as a discretionary courtesy or service and not a right of yours nor an obligation on our part-approving your reasonable overdrafts. As an alternative, you may initiate an automatic transfer authorization to have funds transferred from another account at the Bank to cover an overdraft. Normally, we will not approve an overdraft for you in excess of your limit including any overdraft handling charge(s). We may refuse to pay an overdraft for you at any time, even though we may have previously paid overdrafts for you. You will be notified by mail of any non-sufficient funds items paid or returned that you have; however, we have no obligation to notify you before we pay or return any item. The amount of any overdraft plus our overdraft or non-sufficient funds charge(s) of $20.00 each time an item is presented that you owe us shall be due and payable upon demand. If there is an overdraft paid by us on an account with more than one (1) owner on a signature card, each owner, and agent if applicable, drawing/creating the item creating the overdraft, shall be jointly and severally liable for such overdraft, plus our overdraft or non-sufficient funds handling charge(s) of $20.00 per each time an item is presented. You may be able to access your overdraft checking limit through a teller, ATM, ACH, check or debit card purchase.

LIMITATIONS: Available to accounts in good standing. If the overdraft checking service is suspended on three occasions in a 12-month period, the overdraft checking service will be revoked for a period of at least six months. The fees charged for the items paid into overdraft or returned, as well as the amount of the overdraft item(s), will be subtracted from the disclosed overdraft protection dollar limit. The order in which transactions are received and processed can affect the total amount of overdraft fees incurred by a customer. First Whitney Bank & Trust reserves the right to limit participation to one account per customer and to discontinue this product at any time with prior notice. Please advise a Customer Service Representative if you do not wish to have this service available on your account.

AUTOMATIC TRANSFER SERVICE

You simply authorize us in advance in writing to automatically transfer funds from one of your other accounts to cover any overdrafts.

• Save expensive returned check charges

• Avoid the embarrassment of a returned check

• Maintain your good credit rating

Ask any of our tellers for details.

TRUST DEPARTMENT SERVICES

- Conservatorships

- Escrow Service

- Executorships

- IRA Burial Trusts

- Health Savings Accounts (HSA)

- Specific Trust Administration

INDIVIDUAL RETIREMENT ACCOUNT

We offer you three options on your IRA account.

(1.) A six month money market certificate with a minimum deposit of $2500.00, paying the current rate of interest at the time of purchase until maturity. This could be a rollover from an already existing retirement plan at some other institution.

(2.) A certificate of deposit up to 60 months with a minimum deposit of $500.00 paying the current rate of interest at time of purchase until maturity.

(3.) A variable rate savings account based upon the six month money market certificate rate. This means that your account will change its rate of interest on the first day of each month determined by what rate the six month money market certificate is at that time. There is no minimum deposit for this type of savings account, which means one could make monthly deposits until they reached their maximum contribution for the year. This savings account will mature in 18 months from the date of the first deposit.

HEALTH SAVINGS ACCOUNTS

We offer Health Savings Accounts at the Bank. Your funds are put into a variable rate checking account in which the interest rate can change quarterly. The interest rate will be determined by the 36 month certificate of deposit rate on the 1st day of each quarter.

Interest begins to accrue on the day of deposit for both cash and non-cash items.

Interest is compounded and credited monthly to the account.

If you close your account before interest is credited, you will receive the accrued interest.

We use the daily balance method to calculate the interest on your account. This method applies a daily periodic rate to the principal in the account each day.

There is no minimum balance to be maintained in this account.

There are no fees on this account.

There are no limitations as to the number of transactions per month.

COMMERCIAL FUNDS TRANSFERS-UCC 4A

Credit given by us to you with respect to an automated clearing house credit entry is provisional until we receive final settlement for such entry through a Federal Reserve Bank. If we do not receive such final settlement, you are hereby notified and agree that we are entitled to a refund of the amount credited to you with such entry, and the party making payment to you via such entry (i.e., the originator of the entry) shall not be deemed to have paid you in the amount of such entry.

Under the operating rules of the National Automated Clearing House Association, which are applicable to ACH transactions involving your account, we are not required to give next day notice to you of receipt of an ACH item and we will not do so. However, we will continue to notify you of the receipt of payments in the periodic statement we provide you.

We may accept on your behalf payments to your account which have been transmitted through one or more Automated Clearing Houses (ACH) and which are not subject to the Electronic Fund Transfer Act and your rights and obligations with such payment shall be construed in accordance with and governed by the laws of the State of Iowa as provided by the operating rules of the National Automated Clear House Association, which are applicable to ACH transactions involving your account.

REG GG DISCLOSURE PROHIBITION OF FUNDING OF UNLAWFUL INTERNET GAMBLING

In accordance with the requirements of the Unlawful Internet Gambling Enforcement Act (UIGEA) of 2006 and Regulation GG, this notification is to inform you that restricted transactions are prohibited from being processed through your account or relationship with First Whitney Bank & Trust. Restricted transactions in which a person accepts credit, funds, instruments or other proceeds from another person in connection with unlawful Internet gambling.

NOTICE: First Whitney Bank and Trust is not responsible for and has no control over the subject matter, content, information, or graphics of the web sites that have links here. The portal and news features are being provided by an outside source – The bank is not responsible for the content. Please contact us with any concerns or comments.